Which Are The Best Chinese Stocks To Watch In 2022?

Summary

- 2021 has been a painful year for shareholders of Chinese stocks in general. Could they be the proverbial coiled springs ready to be released in 2022?

- I identified Alibaba Group, NetEase, Tencent Holdings, Baidu, and JD as the five watchlist members.

- The quant ranking and rating of the five stocks are discussed.

- I recognize that market players need to be convinced that Beijing is not out to ‘kill’ the private sector.

- Hence, I shared key developments recently that could help with debunking that narrative.

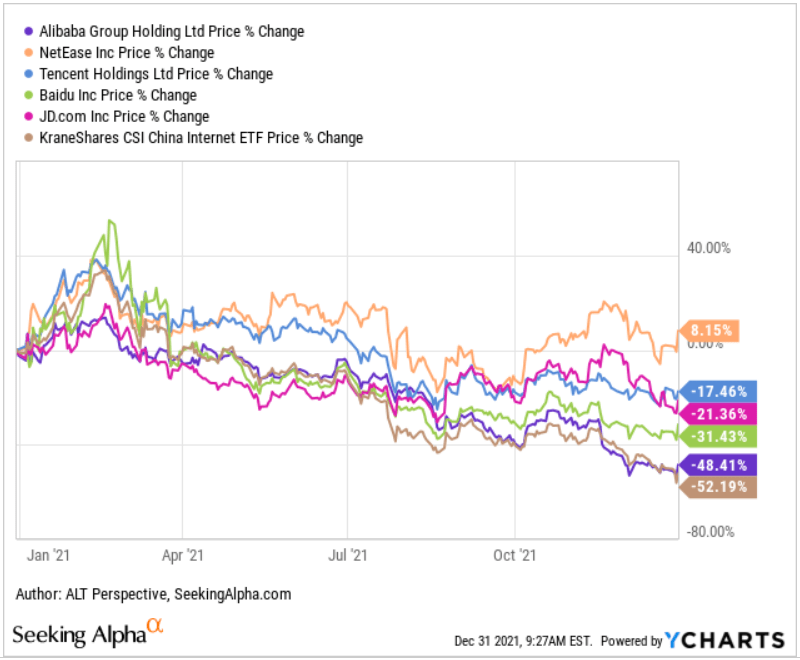

How Did Chinese Stocks Do In 2021?

2021 has been a painful year for shareholders of Chinese stocks in general. Alibaba Group Holding Ltd had appeared to be the sole target of Beijing after the authorities scuttled the initial public offering [IPO] of its fintech arm, Ant Group. The trigger was often attributed to a scathing speech by its founder Jack Ma decrying that outdated regulations had been hobbling the fintech industry.

That belief, coupled with the positive momentum for tech stocks and a boost for certain Chinese internet stocks by some massive buying of Bill Hwang’s family office Archegos, helped push the sector to a crescendo in February. Archegos’ leveraged bets subsequently unraveled amid a heightened regulatory environment that had widened beyond Alibaba Group.

The double whammy quickly evaporated the early 2021 gains for many U.S.-listed Chinese ADRs. Thereafter, three main drivers resulted in the unabated selling of these stocks: i) delisting concerns due to the much-hyped Holding Foreign Companies Accountable Act [HFCAA], ii) the decimation of the for-profit after-school tutoring industry virtually overnight, as well as iii) trumpeted fears of a potential repudiation of VIEs by the Chinese government resulting in the Chinese ADRs losing all their value overnight.

As a shareholder in several Chinese ADRs and a writer covering the sector, I have sought to dispel what I believed to be unfounded attacks on the related stocks. I explained in Chinese Internet Weekly: Mea Culpa that my experience with stocks like Chipotle Mexican Grill and Crocs left me ingrained that I should stay the course with stocks that experience unjustified market pessimism.

Unfortunately, this had not helped with the case of Chinese stocks as the ‘voting machine’ mode is stuck and the ‘weighing machine’ mode did not get turned on after more than a year. The Chinese Internet sector representative ETF, the KraneShares CSI China Internet ETF, inevitably lost favor among investors, declining by more than half from end-2020.

BABA stock, the face of the Chinese internet sector, led the bloodletting among the bigger names. Despite already being ‘discounted’ coming into 2021, BABA went on to lose nearly half its price through the year.

The outperformance of NetEase deserves mention because the company’s core gaming business was negatively impacted by a suspension in games approval while a key arm, Youdao, was dragged into the sell-down of edtech names. NTES stock managed to post an 8.2 percent gain from end-2020, albeit thanks to a big bounce on the penultimate trading day of 2021.

Best Chinese Stocks To Watch In 2022

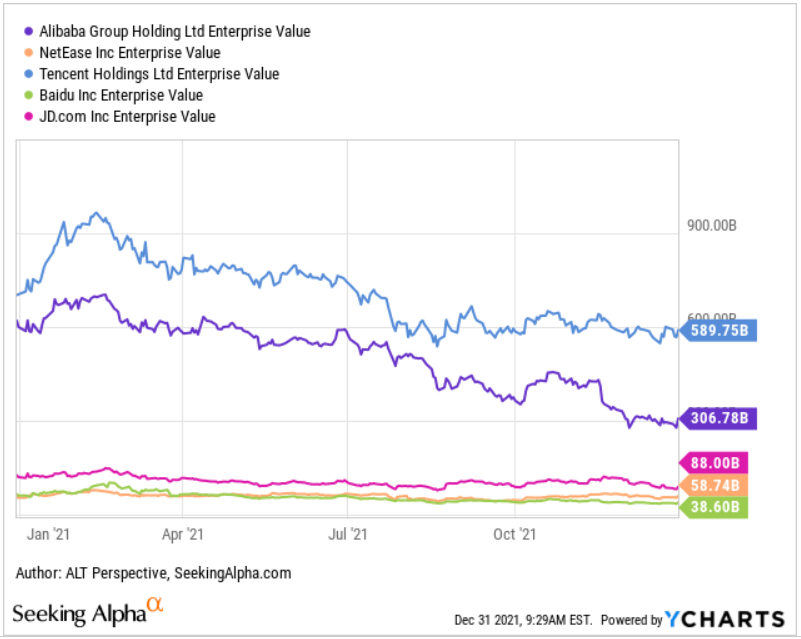

By now, you may have guessed that the five large caps I have chosen to be the “Best Chinese Stocks To Watch In 2022” are those displayed in the price change chart. They are namely: Alibaba Group, NetEase, Tencent Holdings Ltd, Baidu Inc., and JD.

One key reason for the selection is their hefty enterprise values which fall between US$38.6 billion to $589.8 billion, placing them among the largest of Chinese stocks with listings in U.S. exchanges. Their large size may have placed them as targets for regulators. However, when the dust is settled, the big players have a much better chance to survive and take a bigger pie of a still growing market. For instance, the suspension of new game titles approval since July has contributed to the deregistration of 140,000 small studios and gaming-related firms in China. This implies that the remaining players like Tencent and NetEase should benefit from the consolidation.

Despite fears of slower business growth amid the regulatory crackdowns and a weakening in the macroeconomy, four of the five selected companies have seen significant increases in their free cash flows over the past year. The strong free cash flow generation should help with their commitments to the ‘common prosperity’ drive Beijing has been pushing over the past months.

Baidu is the sole contender here which has seen its free cash flow decline. However, as I elaborated in Baidu Stock: What To Watch For Going Into 2022, Baidu is relying on its “Do Better with Tech” approach to help it get into Beijing’s good book, rather than relying on cash donations. Its investments into autonomous driving, cloud computing, and artificial intelligence have also seen early fruits of success.

Besides strong cash flows and large enterprise values to ensure their survivability, these five companies are ‘standalone’ companies among the giants. In other words, they are not owned by another large Chinese internet company which would subject them to the risk of divestment as we have seen with Meituan, Pinduoduo, KE Holdings, Sea Limited, and Kuaishou Technology.

These five companies have a common backer – Tencent Holdings – and were heavily sold off recently due to investors’ fear that the social media and gaming giant would further divest its investments as it had done with JD and Sea Limited in the past weeks. They were selling ahead of an overhang on those stocks, as though creating a self-fulfilling prophesy.

JD, part of the five selected stocks here, used to have Tencent as the majority shareholder but the latter has since announced the distribution of the shares it owned. Hence, it is believed that the current share price has already reflected the news. Looking from the perspective of the KWEB ETF, my five shortlisted stocks are the top 15 KWEB holdings that aren’t backed by another Chinese internet titan.

Source: KraneShares

In the following section, I will look at each of the five stocks from the quant perspective.

Alibaba Group Holding Limited

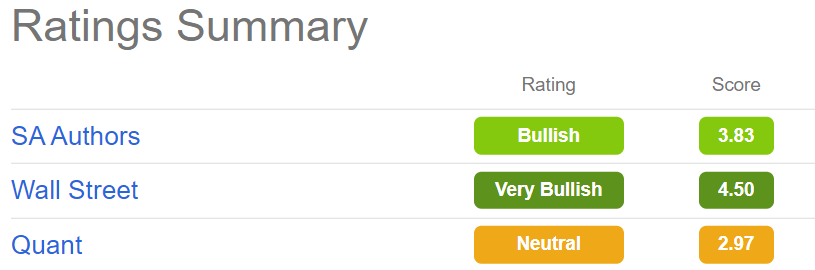

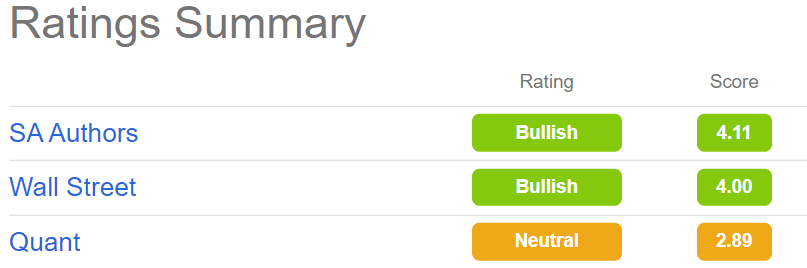

Considering the more vocal bear camp and the dismal share price performance of BABA in the past year, it may be surprising to know that authors on Seeking Alpha are predominantly sticking to a ‘bullish’ rating. BABA has a consensus score of 3.83 out of 5 from SA authors.

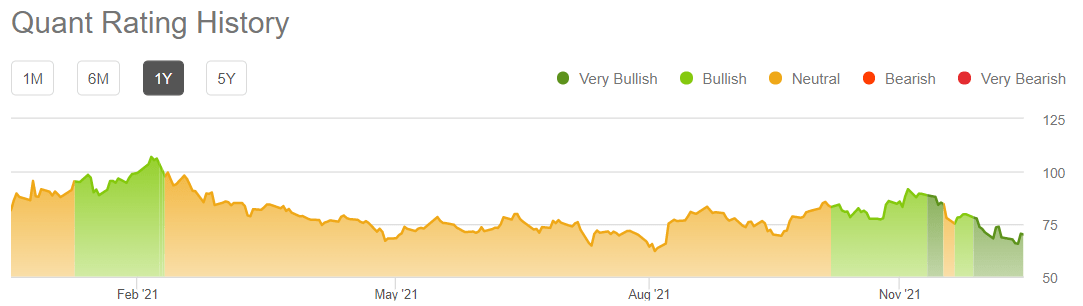

It may be even more baffling that Wall Street analysts remain ‘very bullish’ on the embattled BABA stock. In this respect, the quant rating of ‘neutral’ seems to be raining on the bulls’ parade.

Source: Seeking Alpha Premium

Interestingly, since the quant rating was downgraded from ‘very bullish’ to ‘neutral’ on November 30, 2020, it has been unchanged. In other words, the quant system has never turned bearish on BABA even as the stock continued to tumble.

Source: Seeking Alpha Premium

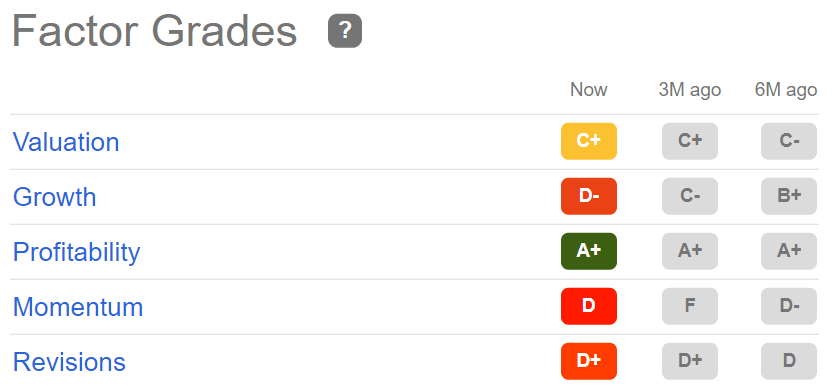

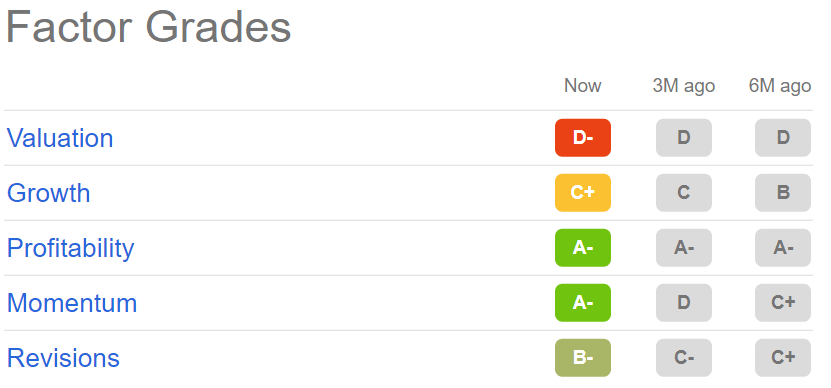

It is important to note that the overall quant rating is not an average of the factor grades listed. Instead, it gives greater weight to the metrics with the strongest predictive value. Given that BABA managed to hold on to its ‘neutral’ rating despite three ‘D’ factor grades, perhaps it has much to thank for the ‘A+’ factor grade it received for profitability.

Source: Seeking Alpha Premium

After all, we know with the sustained downtrend in BABA, a ‘D’ grade for momentum is to be expected. The same goes for its declining growth rate and downward revisions over the past year. With the share price falling more than fundamentals, BABA avoided a worse grade for valuation.

Despite its outsized woes, Alibaba Group is ranked 8 out of 46 companies in the Internet and Direct Marketing Retail industry as of December 31, 2021. It is ranked 236 out of 465 companies in the Consumer Discretionary sector.

Alibaba’s consensus EPS revision trend has reversed to an upward increase in December, following months of decline. Perhaps Wall Street has finally deemed their cuts adequate. If the analysts continue to raise their forecasts, the revision factor grade could improve and trigger an upgrade to BABA’s quant rating. BABA stock’s relative resilience since the beginning of the year will help analysts tell a story of improved sentiment and should make them confident of increasing their forecasts.

Source: Seeking Alpha Premium

JD.com, Inc.

Of the five watchlist members, JD is the only one with a quant rating of ‘very bullish’ (score of 4.58 out of 5). In fact, there isn’t anyone with a ‘bullish’ rating, with the rest given a ‘neutral’ rating. Hence, JD is a true standout. SA authors and Wall Street analysts expressed the same level of bullishness for JD as for BABA.

Source: Seeking Alpha Premium

JD’s ‘very bullish’ quant rating came despite having three C-rated factor grades – valuation, growth, and momentum. It does have two other A-rated factor grades though – profitability and revisions. Recall that the overall quant rating is not an average of the factor grades listed. Rather the metrics with the strongest predictive value have a greater weight. Also, we should note that JD has its factor grade for revisions upgraded from D+ to A, a substantial jump, in a span of three months, and despite ongoing regulatory headwinds facing Chinese internet stocks.

Source: Seeking Alpha Premium

JD was upgraded to ‘very bullish’ from ‘bullish’ only on December 13, 2021. On that day, JD stock closed at $78.05, 11.4 percent above the $70.07 it ended 2021. Nevertheless, perhaps we need to give JD’s quant rating more time to prove itself.

Source: Seeking Alpha Premium

According to Seeking Alpha, its ‘Very Bullish’ quant recommendations “represent the culmination of powerful computer processing and ‘Quantamental’ analysis. The backtest trading strategy shows the effectiveness of our autonomous Very Bullish stock selection model.”

It bears noting that the backtested strategy has proven to yield impressive returns compared to the S&P 500, over the last 10-years. It has outperformed the market nine out of 10 years.

JD now ranks first of 46 companies in the Internet and Direct Marketing Retail industry as of December 31, 2021. It is ranked 49 out of 465 companies in the Consumer Discretionary sector, ahead of Alibaba.

NetEase, Inc.

NetEase has a diversified business and a profitable gaming franchise. Again, like JD and BABA before it, SA authors are ‘bullish’ on NTES stock while Wall Street analysts are ‘very bullish’. The quant rating for NTES is ‘neutral’ with a score of 3.03 (out of 5).

Source: Seeking Alpha Premium

NetEase’s neutral rating comes at somewhat of a surprise given its superior factor grades compared with the other three on the watchlist (apart from JD). It has an ‘A-‘ for both profitability and momentum. On momentum, the ‘A-‘ was a big leap from the ‘D’ it received three months ago.

NTES also has a fairly decent ‘B-‘ for revisions, up from the ‘C-‘ it received three months ago. Even as analysts were busy lowering their forecasts for other Chinese internet stocks, NTES saw upward revisions in the past months.

Source: Seeking Alpha Premium

Tencent Holdings Limited

Among the five watchlist constituents, Tencent is the least favored among Wall Street analysts, earning only a ‘bullish’ consensus rating. The other four, to the disbelief of bears, have ‘very bullish’ ratings.

Source: Seeking Alpha Premium

TCEHY’s ‘neutral’ rating for quant is somewhat obvious, given the poor factor grades it received for valuation, growth, momentum, and revisions. Its saving grace is the ‘A+’ grade for profitability. After all, the social media and gaming giant is still a monstrous profit generator, despite the challenges in 2021. Its net income on a twelve-month trailing basis (Q4 2020 to Q3 2021) was $29.3 billion, up from just $2.0 billion in 2012.

Source: Seeking Alpha Premium

Tencent is ranked 21 out of 50 companies in the Interactive Media and Services industry. It is ranked 108 out of 206 companies in the Communication Services sector.

Baidu, Inc.

Baidu’s ratings profile is the same as Alibaba and JD. It has the lowest quant score among the five watchlist members at 2.76 though the small differences at the one decimal place magnitude most probably aren’t meaningful.

Source: Seeking Alpha Premium

BIDU’s factor grades aren’t remarkable but it’s worthy to point out that all five watchlist members have at least an A- for profitability.

Source: Seeking Alpha Premium

In the same industry and sector as Tencent, Baidu ranks lower for both. Baidu is ranked 24 out of 50 companies in the Interactive Media and Services industry. It is ranked 131 out of 206 companies in the Communication Services sector.

Bottom Line

Of course, for the fundamentals (and quant ratings) to matter, I believe market players need to be convinced that Beijing is not out to ‘kill’ the private sector and U.S.-China tensions should ameliorate substantially. On the former, it is important to realize that regulators around the world are studying how to rein in the big tech companies, particularly on antitrust matters. Beijing is not alone.

News of U.S. and foreign governments considering ways to penalize Facebook, Alphabet’s Google, and Amazon among others, make the headlines every week. However, because the Chinese government managed to get its message across to the companies quickly and imposed penalties effectively soon after announcing investigations on the offending parties, market players deemed Beijing as anti-capitalist, that they are going to nationalize the private enterprises.

Several readers shared that their reluctance in investing in Chinese stocks stemmed from what they deemed as a one-man rule in China making their stock analysis meaningless. If the Chinese president can arbitrarily ‘attack’ the companies on a whim, all bets are off.

However, while there may have been a sea (Xi) change since Xi Jinping became China’s leader, it’s not like he can always bulldoze his way through all policies. A recent Nikkei article noted “an unusual commentary was published in the People’s Daily, the mouthpiece of the Chinese Communist Party.” The commentary was a rare piece with no mention of Xi, the party’s general secretary and China’s president.

In the eyes of those who believe Xi is out to proclaim he’s a more paramount leader than Deng Xiaoping, it must seem outrageous that the commentary even heaped praise on the latter and referred to him by name nine times. In fact, in the Chinese Communist Party’s third resolution since its founding 100 years ago which was adopted in November, Deng Xiaoping’s program of market liberalization known as “reform and opening” was extensively attributed as a key driver for China’s success.

The third resolution was adopted at the Sixth Plenum of the Communist Party’s 19th Central Committee, an event that received generous media coverage globally in the weeks prior. The phrase “reform and opening” was mentioned 29 times, a clear repudiation to analysts who claimed that Xi would downplay Deng’s achievements and make known his desire to reverse the market liberalization.

The full text of the third resolution cited Xi’s acknowledgment of reform and opening in a 2018 speech marking the 40th anniversary of the launch of that policy at the 1978 Third Plenum:

“On the 40th anniversary of the launch of reform and opening up, the Party held a grand ceremony to mark this important event. In his address at the ceremony, Comrade Xi Jinping reviewed the great achievements made and valuable experience accumulated over those four decades. He stressed that reform and opening up represented a great awakening for the Party and a great revolution in the history of the Chinese nation’s development, and he called for continued efforts to see this process through.”

In short, it seems Beijing is not reversing its policy and going on a campaign to nationalize private entities as some critics charged. Even if Xi Jinping does have strong statist tendencies, the third resolution suggests a powerful pro-market faction exists within the party leadership to restrain the president.

Meanwhile, investment experts are seeing signs of the heavy-handed crackdown ameliorating in 2022. Thomas Poullaouec, head of Asia-Pacific multi-asset solutions at T. Rowe Price, said in a note to clients that Beijing has “hinted it would go easier on regulating big private sector players” and that “excessive capital growth may instead be curbed through other mechanism.”

I have long argued that regulatory crackdowns may not always be detrimental to the Chinese big tech. I mentioned earlier that many small players could not survive the regulatory winter, leaving the larger companies like Tencent and Alibaba to pick up market share.

Of the five watchlist members, I rank Alibaba Group on top. Incidentally, BABA stock has the highest upside (64.2 percent) based on the consensus Wall Street analyst price target.

In mid-December, I argue in Alibaba: ‘New’ Risk Was Hiding In Plain Sight that the investment blacklist that has ensnared hundreds of Chinese entities is the big hairy monster that BABA shareholders should be in full alert of. Well, if I am wrong about this, and I am often wrong, BABA stock could enjoy a reversal of its downtrend for a prosperous 2022 and beyond.

Last week’s news about Alibaba discussing a sale of its 30 percent stake in Weibo to a state-owned media company could mark the beginning of its divestment phase. Shedding non-core assets would make Alibaba less of a regulatory target and enables the company to redeploy the funds for more productive purposes. I believe this is a key area that shareholders should monitor.

Author: ALT Perspective, Seeking Alpha