Stronger U.S.-China Ties Could Mark The End Of The Chinese Bear Market

Summary

- One of the most critical obstacles between U.S. and China relations has been removed.

- U.S and China are following through some of the commitments made from the Tianjin Meeting of July 2021.

- The ongoing developments of the Taiwan Question could still weigh on market sentiment.

- FXI’s largest holdings are positioned to be broadly diversified and take advantage of China’s growing economy with the middle class, absent a Black Swan event.

- CQQQ and KWEB are the best plays for a high-beta Chinese Internet Rebound.

When does the pain stop? A better question is, when does FOMO begin?

This entire year has been challenging for Chinese equities, and we are now witnessing multi-year lows in the major Chinese ETF FXI, which includes exposure to Chinese Internet, Real Estate, Financial Services, and Consumer discretionary. Along with crown jewels Alibaba and Tencent, the FXI ETF and the more internet sensitive ETFs KWEB and CQQQ have seen severe net institutional investor selling despite continued inflows into these ETFs.

Sentiment has turned from traditional investor bearishness to near total cynicism and deep distrust towards China’s political and economic situation. FXI, which is one of the best proxies for large-cap Chinese equities, has unsurprisingly borne the brunt of the depressed sentiment and is now sitting at prices not seen since the lows of the 2020 pandemic.

Rather than observe traditional investments commentary towards Chinese equities such as the “outlook has diminished” or “earnings revisions could be negative”, a new wave of thinking has emerged – that “Chinese equities are totally uninvestable” or that the “CCP cannot be trusted to handle a free-market economy.” These comments are easily found on all forms of social media ranging from YouTube, Twitter, to even comments here on Seeking Alpha.

In this research piece, I want to demonstrate that we could be nearing a turning point for U.S. and China relations to improve from this point forward. And as a result, I wish to illustrate that substantial opportunities for alpha await patient investors. FXI is an ETF that tracks Chinese Large Cap growth with exposure to sectors such as Consumer Discretionary, Internet, Real Estate, and Insurance and is one of the best ETFs to gain exposure to any broad-based rebound in Chinese equities. For anyone looking for exposure to sharper higher risk/higher reward rebounds in the Chinese Internet, I would also recommend KWEB and CQQQ.

With nearly all retail and institutional investors underweight Chinese equities, any potential upcoming rebound is likely to catch many investors and short-sellers by surprise.

The Political Situation: Relations are improving, but risks are still high

The relationship between the U.S. and China has always been a sensitive topic for both readers in the West and the East. Given the intense race to become the leading economies in the world, the U.S. has taken a very hawkish approach towards China, a view that was accelerated under President Trump’s presidency. While there was hope that President Biden would seek mutual cooperation with China, so far since he has held office he has maintained Trump’s hawkish stance by keeping trade tariffs in place while keeping ramping up pressure on issues related to Hong Kong, Taiwan, Intellectual Property, among other issues.

In fact, it’s possible that one could view President Biden as even more hawkish on China than former President Trump. President Biden’s appointments of close aides to advise on China have included individuals who have had historically a tough stance on the issue. His appointment of Indo-Pacific Coordinator Kurt Campbell is a confirmation that Biden most likely will keep pressure on Beijing. Recent actions such as forming a partnership with the UK and Australia for a military alliance to counter China illustrate Biden’s hawkish view on this issue.

Revisiting one very important event that I believe many market participants may not have followed closely enough was the in-person meeting in Tianjin China between the teams led by US Secretary of State Wendy Sherman and China’s Foreign Minister Wang Yi back in the July 25th-July 26th 2021 meeting. During the meeting, China pointed out a “List of U.S. Wrongdoings that Must Stop”. The list from China included the following notes for the US:

- Revoke Visa restrictions from CCP Members and their Families

- Revoke Sanctions on Chinese Leaders

- Remove Visa restrictions from Chinese Students

- Revoke extradition request for Meng Wanzhou

- Stop suppressing Chinese Enterprises, harassing Chinese students, Confucious institutes

- Revoke the registration of Chinese Media Outlets as “Foreign agents” or “foreign missions”

After a very tense summer of diplomatic relations, the political tension may be easing after this past week’s developments. As of Sunday September 26th, Canada has released Meng Wanzhou (Huawei’s CFO) after the U.S. Justice Department allowed Meng to return home to China. Around the same time, China released two Canadian diplomats Michael Kovrig and Michael Spavor to return to Canada. According to media outlets, both Mr. Kovrig and Mr. Spavor were suspected and detained by Chinese officials for espionage.

This development is key for several reasons. Firstly, it removes one of the largest sources of contention that has been in the background of US-China relations since late 2018 and it also represents concrete actions taken since the meeting in Tianjin to improve communication between the two countries.

While only the inner political circles of Biden and Xi will know what precisely happened on the important phone call they had together on September 9th, the news flow in the past couple weeks indicates that there was strong mutual desire to improve frayed relations and to take concrete steps to improve them. It’s likely that Biden and Xi’s phone call discussed the many irritants that have been plaguing Sino-US relations such as the Taiwan Question, and the steps necessary to move forward based on the last conversations from Tianjin.

Sentiment takes time to change, and this recent development with Meng Wanzhou returning to China is undoubtedly a step in the right direction. It goes without saying that this does not necessarily represent the exact bottom for Chinese equities, but could position sentiment to recover in the weeks and months ahead from here.

The U.S. has a strong vested interest in continuing to do business in China

Despite increased talk over the past several months in media outlets on decoupling from the Chinese markets to protect American interests, the truth of the situation remains that both the U.S. and China depend on each other for trade and business.

In a Wall Street Journal interview with the U.S. Commerce Secretary Gina Raimondo, she reiterated that decoupling from doing business in China is not even under consideration. Gina goes on to mention that given the size of the Chinese market, the U.S. must continue trading with China while balancing its interest with national security.

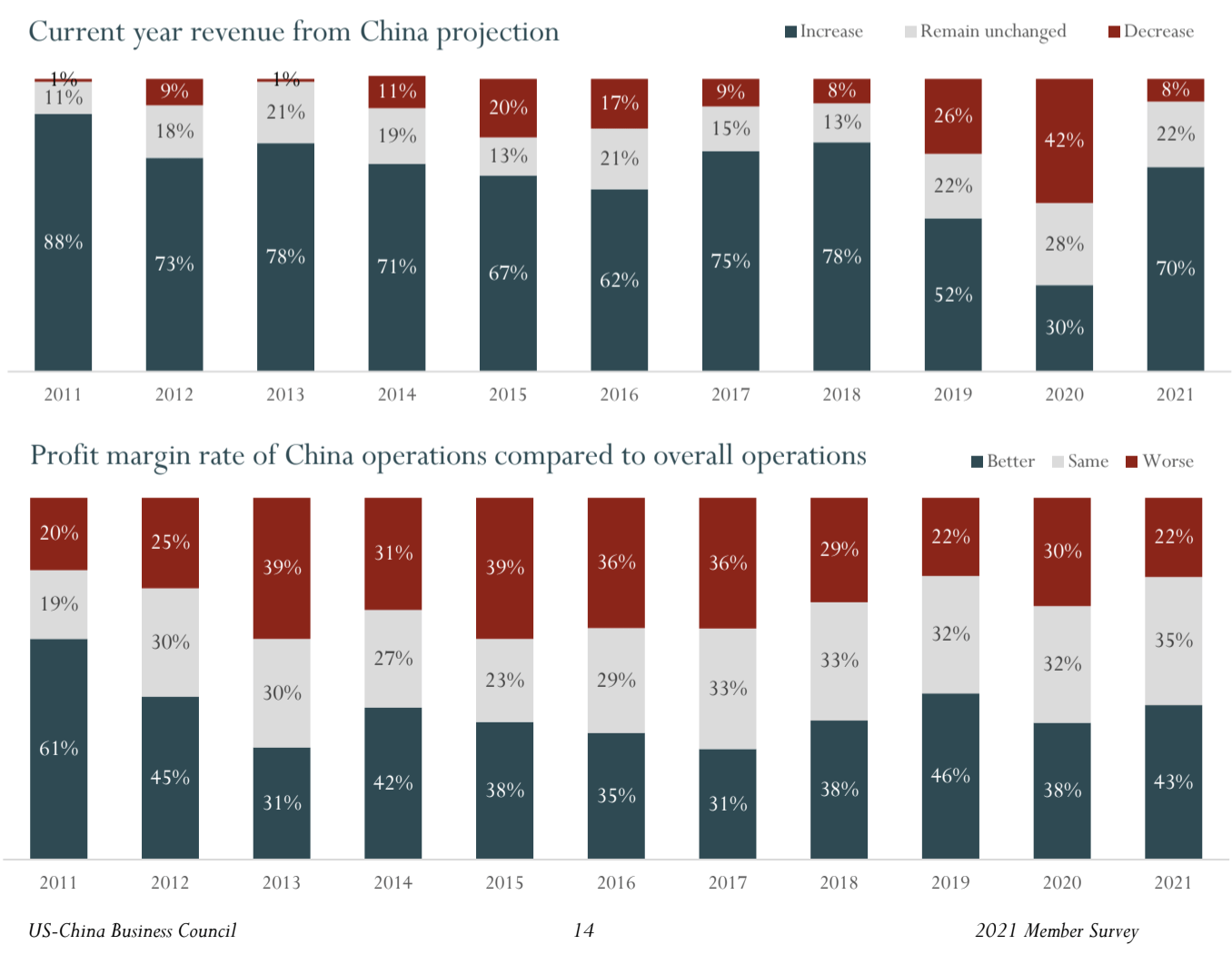

In a recent survey conducted by the US-China 2021 Business Council, an overwhelming 95% of American Companies that do business there continue to report that they are profitable. This observation is noteworthy because profitability continues to be achieved despite the ongoing trade tensions, geopolitical turmoil, and concerns over intellectual property and perceived preference for greater support of domestic Chinese companies.

Source: US-China Business Council 2021 Survey

In addition, a significant number of members of the 2021 China-US business council projected that their business revenue would grow this year from their China operations, which is a large jump from the previous two years. In the second bar chart below, we can observe that profit margins are stable compared to the past several years. This illustrates the strategic importance of the China market and the opportunity cost of not participating in doing business in the second largest economy of the world.

Source: US-China Business Council 2021 Survey

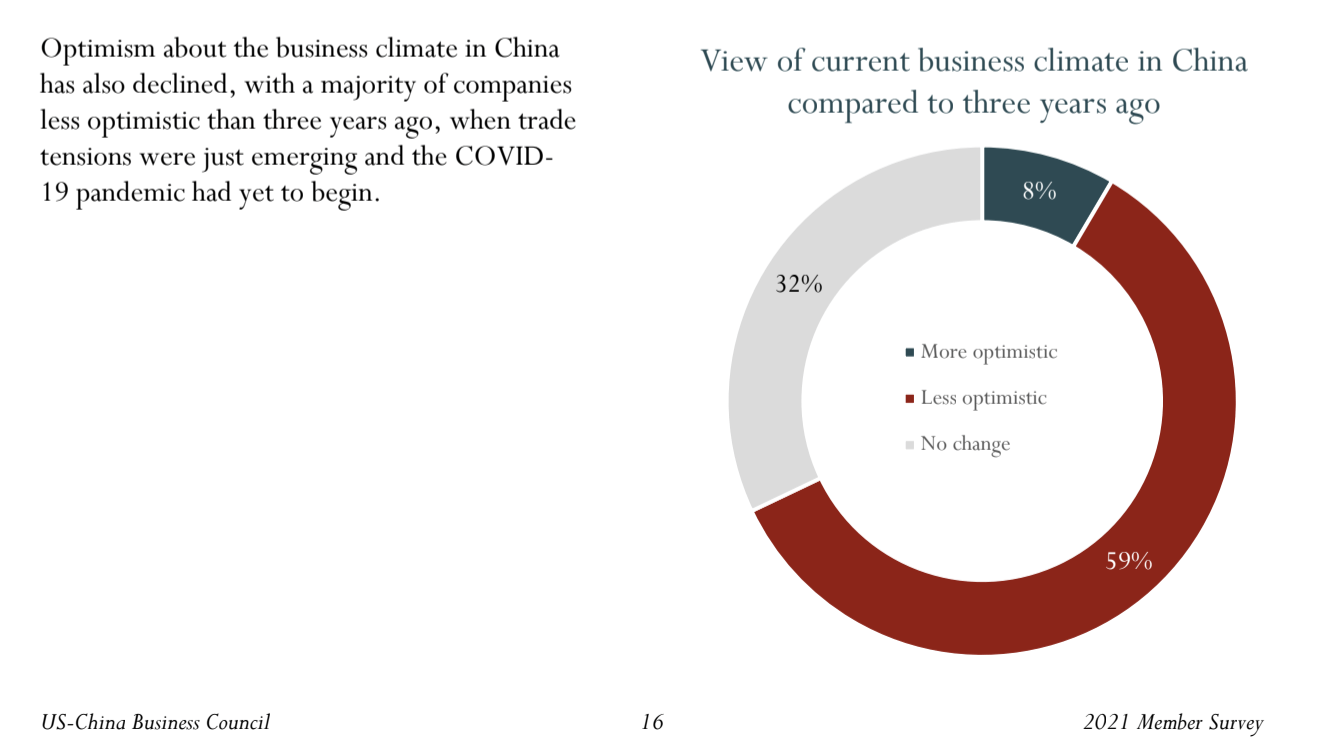

Despite these promising fundamental business developments, it is also worthy to note that the level of optimism for the future of the business climate in China has declined. As seen from the chart below, more than half of respondents are now less optimistic about the business climate. This cautious sentiment makes sense given the elevated hostility between US and China politicians and the growing uncertainty over Chinese regulations on sectors ranging from Education, Internet, Real Estate, Healthcare, among others.

Source: US-China Business Council 2021 Survey

I believe that while the door has been opened to greater mutual cooperation going forward, there are still hidden risks lurking in the background that I wish to bring to my readers’ attention. As we all know, the biggest risk to equity markets and political stability is any potential military conflict between the two great economies of the world. Any escalating military rhetoric is almost certainly provoked by the politics surrounding Taiwan’s perceived independence and how Taipei would seek the defense of other countries – namely the U.S.

While on the September 9th phone call with Xi, Biden expressed his commitment towards the One-China policy. However, shortly after the call ended, we witnessed reports of the U.S. being “supportive” of Taiwan wishing to change its name from “Taipei Economic Cultural Representative Office” to “Taiwan Representative Office.” These conflicting events muddle the true intentions stemming from Washington and are likely to slow down progress with the rebuilding of the US-China relationship. It is important to note that in the past weeks, we have seen the continued presence of China’s PLA (People Liberation Army) fighter jets in Taiwan’s air zone. These demonstrations from China represent its deep commitment in squashing any perception of Taiwan independence, and at the same time, serves as a signal of continued tension in US-China geopolitics.

Although what I’m about to say is just an opinion, I think markets are climbing the proverbial “wall of worry” with the Taiwan Question always in the back of the minds of politicians. I caution my readers against going from full pessimism to experience FOMO in the event of a Chinese equity rebound so long as this issue is in place. Strong, and most importantly, sustainable durable gains are possible only when we have a stronger commitment from the U.S. demonstrating its sincerity on the One-China principle, which I believe will accelerate the healing of China-US relations.

What about Evergrande? Doesn’t that matter?

Evergrande’s crisis has been brought to great attention on social media channels such as YouTube, Twitter, Instagram where I have witnessed the overnight birth of hundreds of new “experts” on the real estate distress in the attempt to chase views and attention.

Underneath the surface of these fear-mongering and highly political videos on Evergrande reveals that very few of the “experts” have any skin in the game as it relates to the situation. If speculators were so sure of the imminent collapse of the Chinese economy, wouldn’t a small short position be a worthwhile wager to demonstrate one’s conviction? Instead, all of the commentary related to the event centered on the skepticism and paranoia related to how China’s economy is built on a house of cards. What we have seen in the past several weeks related to Evergrande has been the emergence of social media news reporters rather than objective, rational analysis.

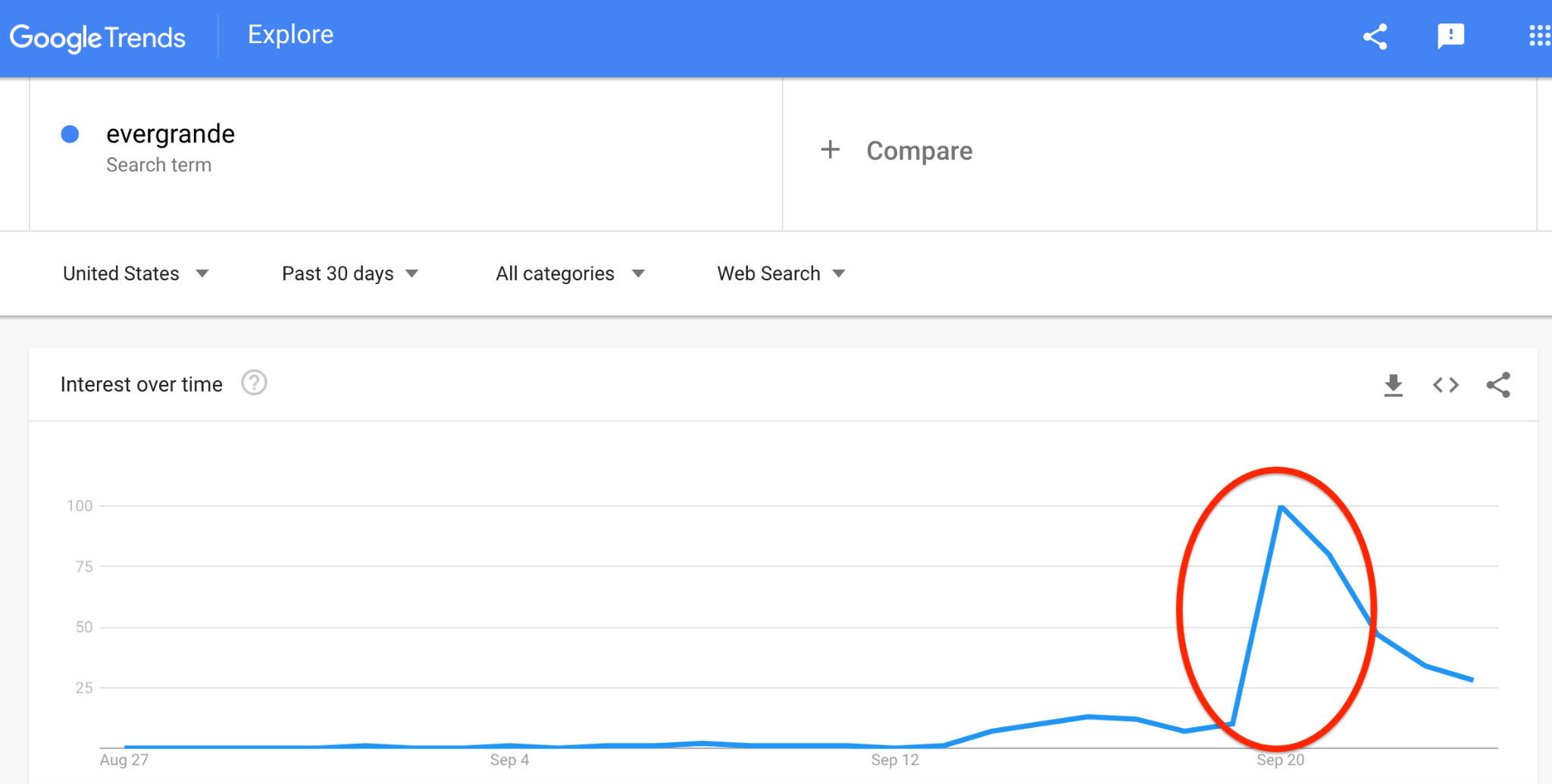

We can see from this image on Google Trends that people have already moved onto the next important topic and that the same social media experts are now focusing on different topics as well. Anyone who subscribed to the fear mongering unfortunately missed the rebound where Tencent reclaimed the psychological $60 mark and Alibaba with the $150 mark.

Source: Google Trends

Near-Term Outlook: Sentiment is a lot better today than it was a few weeks ago but challenges remain.

While it has been a very challenging investing environment for Chinese equities, there continues to be significant opportunities for alpha the moment sentiment stabilizes and investors refocus on fundamentals rather than political risk. In such a case, this rebound could spark fear of missing out (FOMO) and cause a mad rush back into high-quality Chinese internet names.

The iShares China Large-Cap ETF is a diversified ETF with the top three holdings – Meituan, Tencent, and Alibaba – accounting for 25% of the index. For investors who do not have the time to discern between sectors in China, the FXI is likely to have lower volatility (but also less upside) compared to investing in a particular sector.

Given that it’s very difficult to pick the exact company that will produce the most alpha with all the constantly changing variables, I’ve started a new position in FXI with 500 shares, and added onto my KWEB (Total now: 500 Shares) and CQQQ (Total now: 400 shares) positions to take advantage of a potential upcoming broader based recovery should the US-China relationship continue to heal. I’ll be closely watching the continued developments from high level policy makers and their decisions surrounding new regulation and collaboration.

My strategy will be to continue to dollar cost average into these three ETFs over time as picking the exact bottom is anyone’s guess. Thank you for reading, and I’ll see you in my comments section below.

Author: Larry Cheung, CFA. Seeking Alpha