Hello Group Is An Obvious Value Play

Summary

- I initiate my coverage on MOMO, also known as Hello Group, with a strong buy recommendation and a price target of $26.59 per share, implying an upside potential of 158%.

- Hello Group operates two very popular apps — Momo and Tantan — and the company is frequently referenced as the ‘Tinder of China’.

- MOMO’s share price is down 73.4% since its local peak in early 2020 and the stock is now trading at ridiculously cheap metrics.

- MOMO is currently valued at a P/E of 6.71 and a P/B of $0.7.

The thesis in a nutshell

2021 was a tough year for China’s internet stocks. While I definitely have sympathy for existing shareholders who suffered through the decline in value, I think new investors should be excited. There are amazing bargain opportunities available for sale, and I argue the company presented in this article – Hello Group – is definitely one such bargain stock.

MOMO’s share price is down 73.4% since the stock’s peak in early 2020 of $38.80 per share and is now trading at ridiculously cheap metrics. Investors who buy the stock at current levels, at a P/E of 6.71 and a P/B of $0.7, may reasonably expect to be financially rewarded.

Based on highly convincing financial data, I initiate my coverage on MOMO with a base-case price target of $26.59 per share, implying an upside potential of 158%.

About Hello Group

Hello Group is one of the leading players in China’s online social and entertainment space. The company operates the two popular apps — Momo and Tantan—, which are designed to enable users to discover new relationships, expand their social connections and build romantic experiences. Hello Group has a very impressive user base. As of November 2021, Momo’s MAU stands at 113.8 million and Tantan‘s MAU at 89.3 million. In the past, specifically since 2018, Momo’s growth slowed and the platform may have reached peak market penetration. Tantan, on the other hand, is still growing and there have been rumors that the app is beating Tinder in some regions in South East Asia such as Thailand and Indonesia. In any case, the financial future of MOMO is likely not based on user growth, but on higher monetization of the company’s existing user base. Currently, Hello Group is generating most of its revenues from live-streaming services, where users tip and gift other users/entertainers, and MOMO takes a commission on the transaction.

Very bullish financial data

What attracted me to MOMO stock was the company’s financial data. All three key financial statements – income statement, balance sheet and cash flow statement – exhibit highly convincing numbers.

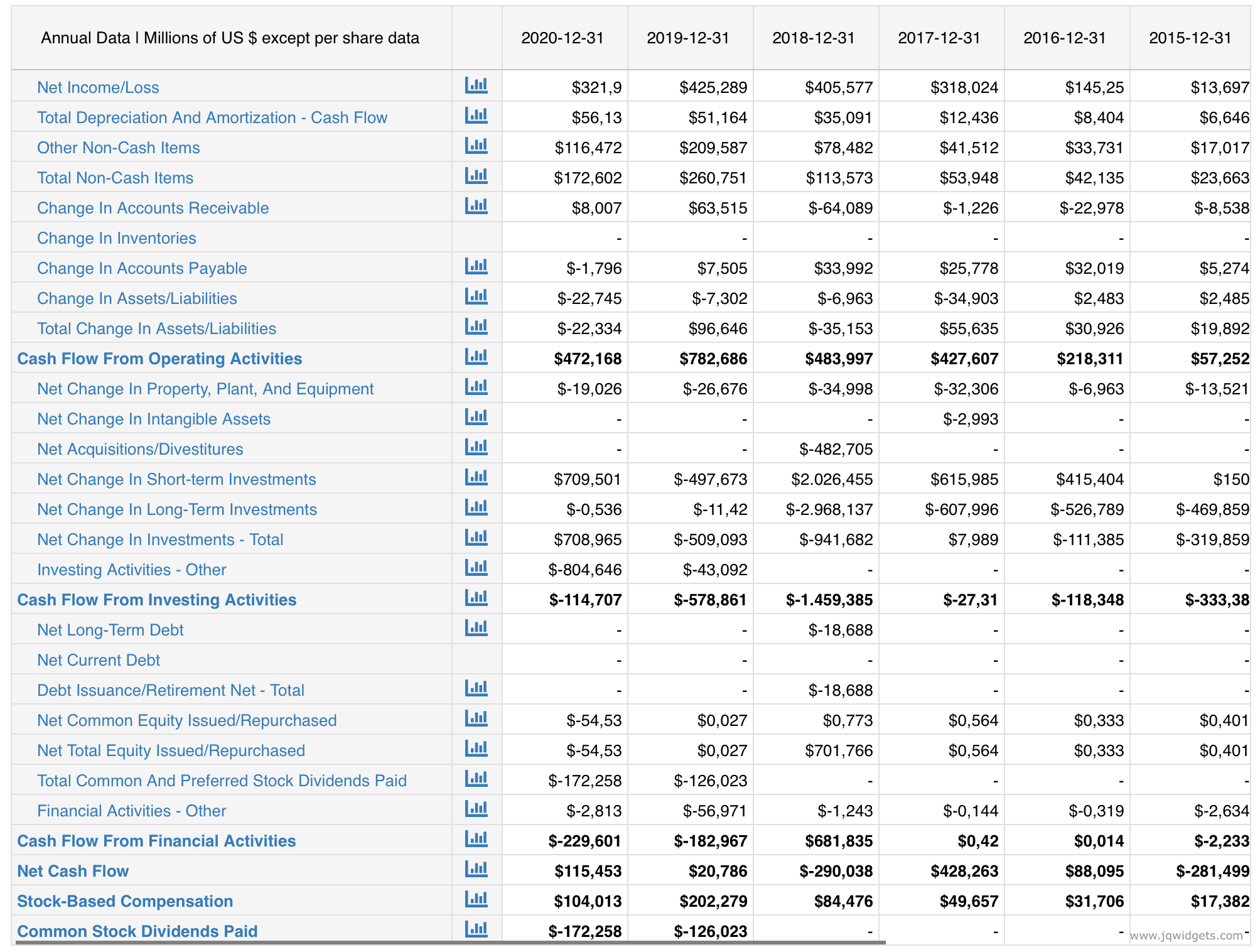

First, let us start with the income statement. In the period 2017 until 2020, revenues grew from 1.318 million to 2.302 million, implying a compounded annual growth rate of 15.02%. Unfortunately, net income did not keep pace with the revenue growth but remained relatively stable at $350 million. According to the management commentary, the lack of profitability growth was due to investments that were allocated to growing the Tantan app. As of Q3 2021, MOMO’s cumulative net profit margin stands at approximately 13.09%.

The cash-flow statement confirms what we have seen in the income statement – a profitable company. As you may note, the cash flow from operations is consistently higher than net income levels, calculating a cyclically adjusted average of +$400 million per year. For reference, MOMO’s market capitalization, as of early February 2021, stands at only $1.800 million.

Another green light is coming from the balance sheet. As of September 2021, MOMO records $1.443 million of cash, which is 78% of the company’s market capitalization. In addition, total debt levels at $1.161 million imply a leverage ratio of less than 1/3 (33%). Thus, in my opinion, MOMO could definitely absorb some multi-year headwinds, while also making considerable investments in long-term growth opportunities.

On September 3, 2020, MOMO authorized a share repurchase program under which the company may repurchase up to $300 million of its shares over the next 12 months. As of September 2, 2021, the company had repurchased 14.15 million ADSs for a total consideration of $182.4 million. Given the high operating cash flow, paired with the $1.400 million cash position, I definitely expect MOMO to continue buying back shares after the current program is concluded.

What is next for MOMO?

Hello Group’s stagnant user base may imply that the company entered the maturity stage, or in other words the monetization stage. Thus, any financial upside potential is likely not driven by a push towards economies of scale, but by more effective monetization of the company’s existing user base. As of Q3 2021, MOMO still generates the major shares of revenues from live streaming services such as virtual gifting and tipping. I think this will likely change. Going forward, I expect MOMO to gradually shift towards more value-added subscription services, similar to Tinder, and ad-sales, similar to Instagram.

In general, I expect MOMO will be able to generate considerable revenues for many years as online dating and online social services remain in high demand. Furthermore, MOMO stands to benefit from the long-term structural shift towards mobile video as the prime choice for online communication and entertainment.

Now available at bargain prices

Every investment opportunity is a function of price. You can turn an amazing company into a bad investment, if you pay too much. Reversely, you can make amazing speculation in an almost bankrupt company if you buy at a bargain price.

From its all-time high in January 2020, the stock has sold off more than 73.4%.

Valuation

Let us now look at what could be a reasonable price target for the company. I have constructed a DCF valuation with a sensitivity analysis of some key assumptions. The results of my analysis are termed Base, Bear, and Bull Case.

Please note the following assumptions:

- I have been very cautious with growth assumptions.

- For the base case, I have attributed MOMO the company’s current EBITDA margins.

- The discount rate used in the analysis is a reflection of the WACC that I have adjusted to account for the different scenarios (risk-free interest rate, inflation expectation and equity / market premium).

- Some further assumptions for the analysis are listed under the respective case

- Of course, feel free to challenge my assumptions.

As you see, possible valuations for MOMO, given the current knowledge about the company, should be between $17.57 per share and $59.84 per share, with $26.58 per share as my Base Case scenario. Since the latest trading price for MOMO has been quoted at $10.31 US, my calculation implies an upside potential of 158%. Personally, I consider the presented opportunity just too attractive to neglect.

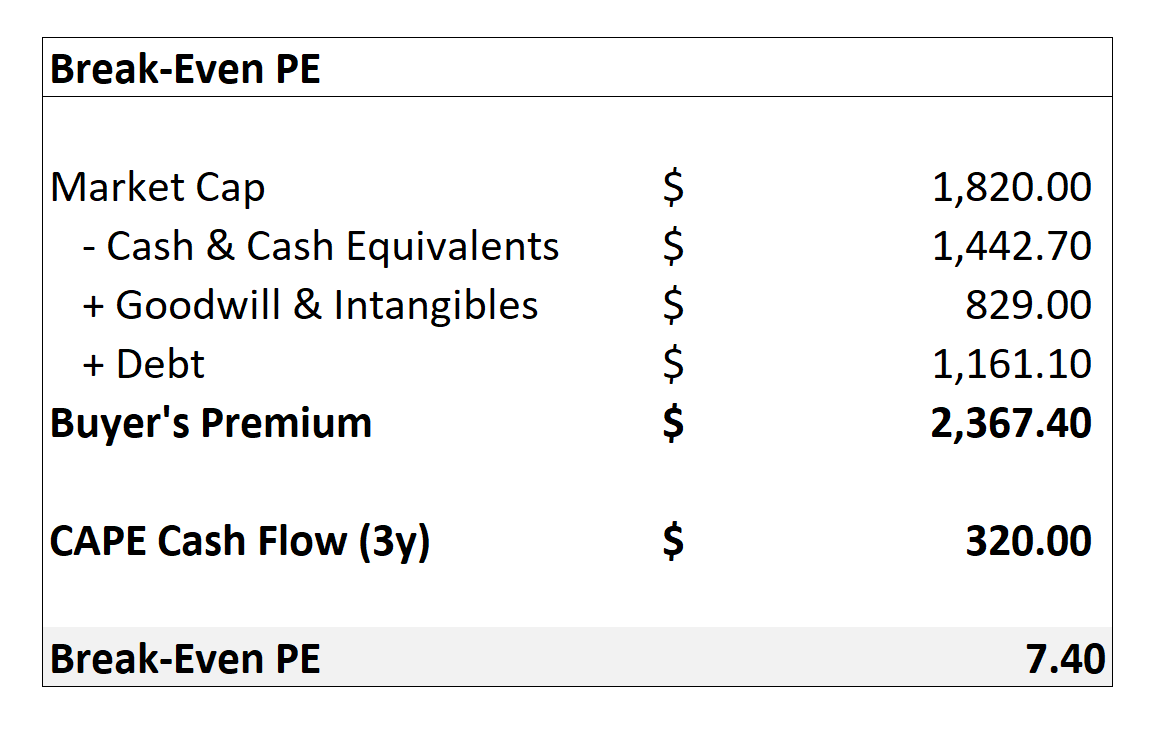

Another way to evaluate MOMO’s current valuation would be an adjusted P/E ratio, that I termed ‘Break-Even P/E’. To understand the metric, first we need to define 3 key terms:

Buyers’ Premium: Market Capitalization, less Net Assets (Tangible Assets – total Debt), less Goodwill.

CAPE Earnings: The 2-3 year average net earnings attributable to shareholders.

Break-Even P/E: Buyers’ Premium divided by CAPE earnings.

Following this calculation for MOMO, we get a ‘Break-Even P/E’ of 7.4. The metric can be regarded as an adjusted P/E and shows how long a MOMO shareholder will need to wait until his capital investment in the company is amortized.

Needless to say: A ratio of 7.4 is very cheap.

Risks and challenges

Although I consider that the market has priced in a lot of negativity for MOMO already, there remain some risks.

Regulatory headwinds in China. The main risk for MOMO stock is arguably regulatory and political pressure coming from the Chinese government. I don’t want to politicize the discussion, or present myself as an expert on China, which is why I would like to encourage every investor to assess the risk-reward of investing in China for himself. For me personally, the valuations of some stocks – especially MOMO – are pushed to such ridiculously low levels that I regard investments in China as justified.

ADR delisting fears. This risk is closely tied to the previous concern of regulatory headwinds. I personally am not afraid of an ADR delisting, but the negative market sentiment and fear could definitely keep the stock price depressed for some time.

Financial shenanigans is another popular risk that many investors cite when reflecting on cheap Chinese bargain stocks. I argue, however, that financial crime is not a problem particular to China, as Wirecard from Germany and Enron from the US exemplified. For MOMO in particular, I would like to highlight three facts: First, the company’s cash position can be confirmed relatively well by tracking the equity issuance history. Secondly, MOMO is buying back shares to underscore their financials. Thirdly, MOMO is audited by Deloitte China — which may give some confidence depending on your view on the BIG 4 auditing firms.

In general, please supplement this article with your own research and invest according to your personal risk tolerance.

Recommendation

At current price levels of $10.31 per share, MOMO is a clear value stock. With reference to a strong balance sheet and highly profitable business operations, I feel confident to give MOMO a strong buy recommendation. My base-case target price is $26.59 per share, implying an upside potential of 158%.

Author: IV Trader, Seeking Alpha