Chinese Internet Stocks: Contradictions Abound And Good News Misconstrued

Summary

- The risks to the economy from a potential collapse in Evergrande are overstated. The purported impact on Chinese Internet stocks is specious.

- Chinese e-commerce platforms could benefit from the mitigation efforts by the government in the ‘rescue’ of Evergrande and the boosting of retail consumption.

- Several contradictions (or hypocrisies) that have left shareholders in Chinese internet stocks scratching their heads are discussed.

- I highlight a few recent good news that were misconstrued as negative developments.

- The return of Huawei’s CFO has been hailed as an important step in the reconciliation of US-China relationship and bodes well for sentiment towards Chinese internet stocks.

Since the previous weekend, investors had been inundated with news of China’s second-largest property developer by sales, and the world’s most indebted, leaving them pondering about the impact on their portfolios. The uncertainties surrounding the potential default of China Evergrande Group spooked market players across the globe.

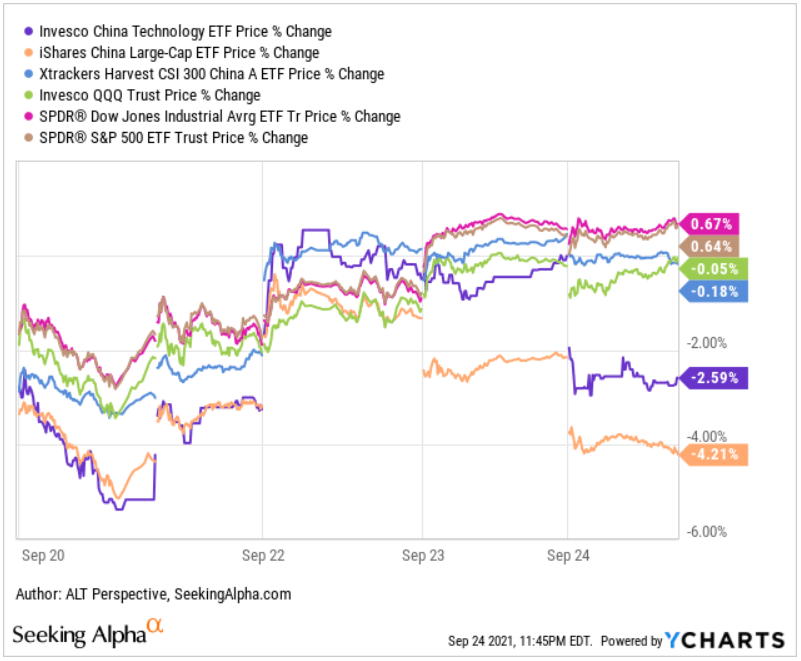

Chinese stocks unsurprisingly bore the brunt of the sell-off amid fears of contagion. Two of the representative ETFs of Chinese companies, the Invesco China Technology ETF and the iShares China Large-Cap ETF, fell more than 5 percent at one point on Monday. The X-trackers Harvest CSI 300 China A-Shares ETF weathered the storm better likely due to its more diversified sector allocation.

The ASHR ended the week relatively unscathed, declining a mere 0.18 percent. The representative counterparts in the United States closed in the range -0.05 percent to 0.67 percent. The CQQQ ETF staged a remarkable rebound to even surpass all the mentioned ETFs for a period mid-week before succumbing to additional negative developments to end the week down 2.6 percent. The FXI ETF was the biggest loser, falling 4.2 percent.

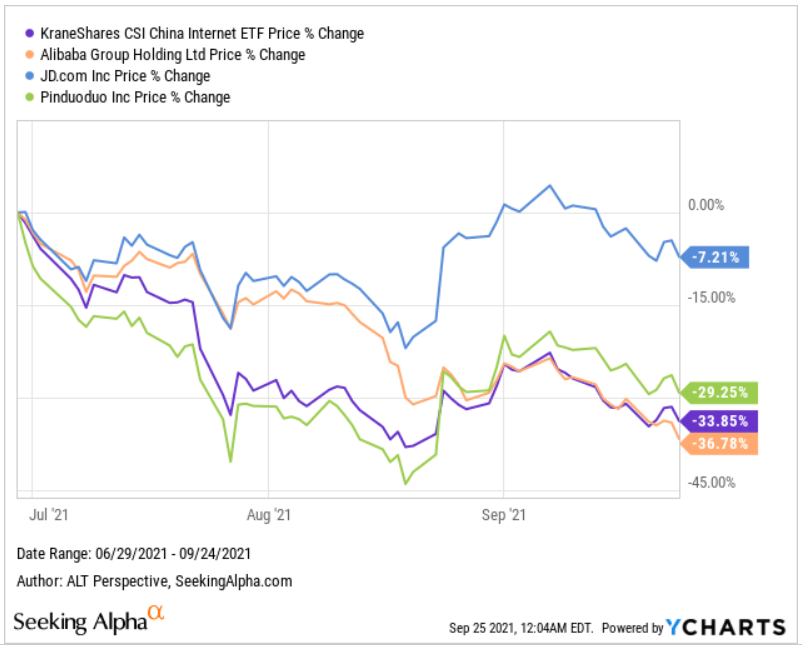

Shareholders of the FXI ETF were probably nervous about the presence of Alibaba Group Holding and JD, as well as two of the largest Chinese banks and Ping An Insurance Group, among the top ten holdings. The former two lost 9.4 percent and 5.0 percent respectively.

The decline in bank stocks was ostensibly due to concerns over bad loans from the Evergrande debacle and the implications from a weaker loan growth if the collapse of the property developer resulted in a domino effect on the economy. Ping An Insurance fell to four-year lows as investors were worried about its property-sector exposure. This was despite the company clarifying that its insurance funds have “zero exposure” to Evergrande and other real estate companies “that the market has been paying attention to.”

In contrast, no banks or insurance companies feature in the CQQQ ETF. The KraneShares CSI China Internet ETF (KWEB), which as the name suggests comprises stocks in the internet sector, fell 3.1 percent for the week. The KWEB ETF was weighed down by the plunge in BABA, Pinduoduo, Bilibili, and JD.

As explained in a past issue of the Chinese Internet Weekly, I found the KWEB ETF holding the most representative stocks in the sector. As such, an overview of the week’s share price movements of the top ten holdings of KWEB (as of Friday) compared with the ETF itself is provided as follows for convenient reference especially for the stocks mentioned in this article.

As I was writing this update, news of the U.S. Department of Justice announcing on Friday that it was dropping charges against Huawei chief financial officer Meng Wanzhou poured in. The unexpected progress in the bank fraud case which had dragged for more than 1,000 days came as Meng reached an agreement with U.S. prosecutors, avoiding an extradition from Canada and allowing her to leave Canada.

Her arrest by Canadian police in Vancouver as she was in transit to Mexico and the subsequent years-long battle to fight against extradition was a central source of discord between Beijing and Washington. Thus, the settlement of the case and her return to China would go a big way to help end a diplomatic stalemate between the U.S. and China.

I expect additional news coverage and analyses on the closure to focus on (or at least touch on) the potentially smoother path of cooperation between the U.S. and China in the coming weeks. Incidentally, a former colleague of mine keenly tracking trade developments pointed out that China’s commerce ministry posted a statement on Thursday that it had terminated an anti-dumping investigation on polyvinyl chloride [PVC] imports from the U.S.

I am not sure if this is merely a coincidence with Meng’s release and whether this is an indication of the Chinese side offering a gesture to the U.S. that it’s ready for a restart on resolving the trade tensions. Whatever the case, more positive news on the U.S.-China relations, whether linked or otherwise, should boost sentiment towards Chinese stocks.

Impact of the Evergrande developments on Chinese Internet stocks

Sentiment on the Chinese internet sector has been very bearish for a while. The use of the term ‘Lehman-moment’ by the media and analysts to describe China Evergrande’s potential bankruptcy evoked bitter memories of the 2008-2009 financial crisis among the investor community and exacerbated fears of systemic risks from its possible collapse.

However, there has been much ink spilled discussing why the comparison is inappropriate. I will briefly share some of the arguments.

First, the panic over Lehman Brothers was in the huge difficulty in determining the value of the financial derivatives it held. Evergrande’s assets are primarily made up of land and housing projects that can be more transparently valued than the opaque and complex financial instruments.

The developer can find willing buyers without offering too steep a discount for its prized land banks as compared to the investment bank seeking to liquidate its fancy credit-default swaps and collateralized debt obligations. The local government might even be happy to buy back the land and re-sell it when the market stabilized.

Second, the beauty of China is the strong control the government has over the banks and businesses. Beijing can communicate with the creditors to arrange a haircut where certain groups like the small firms and house buyers are prioritized for larger payouts while others like investors in Evergrande’s Wealth Management Products, apart from the employees, would be the hardest hit. Equity holders of Evergrande are likely to be wiped out while U.S.-dollar bondholders could see huge losses.

I doubt the authorities are naïve to think it would be easy to rein in excessive risk-taking and high indebtedness in the property sector without some pain in the economy. Instead, I believe Beijing would rather undertake this ‘controlled demolition’ now to avoid even greater complications subsequently. Evergrande’s circumstances are, after all, no thanks to limits on corporate debt that the government issued last year.

Third, the high prices in construction materials provide further impetus for the Chinese government to accept a slowdown in the industry stemming from the failure of Evergrande. A lower import requirement of iron ore, copper, plastics, etc. as a consequence of slower homebuilding amid elevated costs is a positive outcome for China. The development itself would help cool the overheated mining sector.

Chinese e-commerce platforms to benefit from the mitigation efforts in the ‘rescue’ of Evergrande

Meanwhile, the policymakers appeared proactive to contain the economic damage. China’s central bank pumped more liquidity last week by raising its gross injection of short-term cash into the financial system. The Ministry of Commerce also issued a policy notice (content in Chinese) outlining 14 measures aimed at promoting consumption.

The timing didn’t seem to be a coincidence and is in line with the government’s efforts to increase the contribution of retail spend on economic growth. It also fits into the drive to reduce the reliance on construction to boost the GDP.

The policy is targeted at encouraging the purchases of new and second-hand cars, home appliances, furniture and home furnishings, catering services, nightlife, sports-related spending, and imported goods. Among the proposals is a refreshing idea to allow the use of empty housing units as temporary storage places for household appliances and furniture to help residents carry out home renovations.

The notice also mentioned the development of new businesses such as “internet + recycling” and “internet + used goods.” There is no elaboration but I suppose a recent IPO company AiHuiShou International Co. Ltd. fits the bill. This can be gleaned from the 13 percent jump in its share price last week amid a sea of red among its Chinese internet peers.

Source: Google Finance

AiHuiShou describes itself as a leading technology-driven pre-owned consumer electronics transactions and services platform in China. It facilitates recycling and trade-in services, as well as the distribution of devices to “prolong their lifecycle.” Its open platform integrates C2B, B2B, and B2C capabilities.

Despite the recent climb, RERE stock is still nearly half of its peak price of $18.49. Since its public debut on June 18, AiHuiShou has been dragged down by the same sentiment hit following the escalation in the regulatory environment on the Chinese companies. More clarity on the government’s support for Internet-facilitated second-hand electronics and appliances trading as well as recycling could sustain its share price rebound.

Likewise, JD.com as the go-to online retailer in China for electronics and appliances could be a major beneficiary of this latest official policy on stimulating consumption. Compared to Alibaba, JD isn’t known for engaging in monopolistic practices. JD also doesn’t rely on excessive subsidies to attract shoppers in the manner adopted by Pinduoduo.

The emphasis on quality imported goods could benefit Vipshop Holding Limited, a leading off-season luxury goods e-commerce player, and JD, as it has a reputation for superior checks to ensure original branded items are sold on its platforms. The renewed national interest in sports would also benefit JD as the e-commerce platform is a popular channel for consumers to get their sportswear and apparel.

Investors probably recognize this, as we can see that JD stock has weathered the regulatory storm better than two of its fiercest competitors. Its share price is down only 7.2 percent in the last three months while BABA is down 36.8 percent and PDD lost 29.3 percent. The KWEB ETF fell 33.9 percent in the same period. JD’s share price outperformance became more apparent from the second half of August as market players had a better understanding of what Beijing was after.

Incidentally, JD is AiHuiShou’s largest investor with 34 percent of its ordinary shares before its IPO. According to DealStreetAsia, JD had in 2019 merged its pre-owned commodity trading platform Paipai.com with AiHuiShou. JD subsequently led a $530 million Series E round funding with the recycling company. The policy tailwind for AiHuiShou would thus indirectly benefit JD via its equity stake in the online recycler.

Contradictions that leave shareholders in Chinese internet stocks scratching their heads

In the past year, we often hear of reports on how Alibaba Group is a corporate bully. It is thus refreshing to learn that a Chinese court found (content in Chinese) Meituan guilty of forcing vendors to sell exclusively on its platform. The largest food delivery platform in China was fined RMB1 million as a penalty. Ele.me, the next largest player in the field and a unit of Alibaba Group, stands to gain if Meituan changes its monopolistic practices following the ruling.

Chinese companies are many a time been accused of making payments ‘under table’ to get deals done or to avoid government scrutiny. Some readers vocally rejected such investments for moral reasons. Last week, Exxon Mobil, ConocoPhillips, and Chevron were found to have failed to meet a core transparency standard.

The three U.S. oil majors refused to publicly disclose taxes and other payments given to governments in certain countries where they operate. When investors realize that it’s not just businesses from a particular nation behaving this way, they could appreciate sometimes it’s a matter of complying with the local practices.

Similarly, a few readers called an investment in Chinese stocks and the purchase of Chinese goods distasteful for patriotic reasons. Yet, Commerce Secretary Gina Raimondo told the WSJ in an interview the U.S. need to trade with China is “just an economic fact” despite increasing tensions over national security and human rights issues.

Trade would typically benefit both countries and in this case, both the U.S. and China would gain, an outcome that the critics do not like to see. Fortunately, with U.S. officials coming out with rational messaging on the U.S.-China relationship, the negative sentiment towards Chinese stocks could be ameliorated.

Meanwhile, I wonder what investors who claimed that Chinese platform companies like Alibaba Group and Tencent Holdings are ‘evil’ for their censorships have to say about Google. The world’s leading search engine by far had complied with requests from Russian officials to remove nearly 1 million web pages, documents, apps, and videos. Google and Apple Inc. were also revealed to have expunged a voting app from a Russian opposition leader.

These transgressions pale in comparison to Facebook’s shenanigans recently exposed by the WSJ. In a five-part series titled “the facebook files”, the WSJ detailed its findings on how Facebook’s platforms “are riddled with flaws that cause harm.”

Source: The Wall Street Journal

Before the social media giant could catch its breath defending itself over the WSJ’s comprehensive exposé, it was ordered by a federal judge on Wednesday to surrender records related to accounts it shut down in 2018 that were linked to government-backed violence against the Muslim Rohingya minority in Myanmar.

Nonetheless, I don’t come across comments in Facebook articles on Seeking Alpha condemning shareholders of being complicit by owning shares in the company. No one warned potential investors of the moral hazard too.

Even as investors worry about a possible slowdown in the Chinese economy, American businesses reported being optimistic about the future in China. A survey conducted by the American Chamber of Commerce in Shanghai (AmCham) found more than 82.2 percent of the respondents forecast their revenues in the populous country to increase this year. Of particular note, nearly 70 percent of the U.S. firms surveyed expect their revenue growth in China would outpace their worldwide businesses in the next three to five years.

Good news misconstrued as negative developments

On Thursday, a company statement (content in Chinese) by Mango Excellent Media revealed that Ali Venture Capital, the investment arm of Alibaba Group, announced its intention to dispose of its entire stake in the publicly traded media company. Alibaba has a 5.01 percent stake in Mango and is estimated to suffer a loss of RMB2.3 billion ($356 million) if it lets go of its entire holdings at the prevailing price of around RMB41 per share.

The media coverage on this sale has postulated on the seemingly ‘forced’ nature and focused on the realized loss. Yet, despite my extensive reading on the topic, I did not come across any write-ups recognizing the funds freed up from this divestment.

The proceeds could be better deployed into Alibaba’s core businesses. The move would also bring Alibaba closer to Beijing’s good books again. Thus, the oversized sell-off in BABA stock on Thursday and Friday is baffling.

Similarly, Reuters’ scoop that Baidu’s $3.6 billion deal to acquire JOYY’s domestic video streaming business could be thwarted was deemed as a negative for the Chinese internet search giant and artificial intelligence leader. However, it should be noted that Baidu announced the acquisition plans in November.

Nearly a year has passed and the valuations of related stocks have shrunk. The heightened regulatory environment must have negatively impacted YY Live as well. Had the deal gone through, Baidu could be overpaying for the video-streaming platform. Thus, it is a blessing in disguise that Baidu can walk away from the agreement citing the disapproval by China’s antitrust regulator, the State Administration for Market Regulation [SAMR].

Did you come across other contradictions or positive developments misconstrued? Let us know in the comments section! My past articles have attracted valuable inputs and discussions. Looking forward to your participation!

Author: ALT Perspective, Seeking Alpha